AuthorInbest is your all-in-one destination for mutual fund distribution, tax consultation, and tailored insurance advisory services in Kolkata. Archives

April 2024

Categories |

Back to Blog

Fire insurance is something that a property owner spends on. In 2023 alone, Statista recorded that Indian insurers had underwritten premiums of over 239 billion INR. So, you can imagine the massive demand for fire insurance policies in the country. Isn’t it obvious? Fire erupts suddenly and engulfs everything in a property, leaving nothing in its way and causing devastation.

With the best fire insurance policy from a general insurance broker in Kolkata, you are covered against damages and allied perils. However, these policies can be of many types. For a new property owner, it can be confusing to navigate the coverages to arrive at the best-suited one. That’s why this blog has dedicated an entire post on it. Scroll down to learn about each type and make informed decisions to safeguard your property from fire-related damages. Commonly Known Fire Insurance Policy Types from a General Insurance Company Let us start by brushing up on your knowledge of fire insurance a bit. A fire insurance policy is property insurance that provides coverage for damages resulting from fire breakouts. The agreement begins with a policyholder paying a premium to an insurance company and, in return, seeking compensation for the financial losses caused by the blaze. Probably the best thing about it is its coverage, which includes damages from lightning, strikes, riots, explosions, and other related perils. Coming back to the most common types, every general insurance broker in Kolkata identifies the following depending on one’s needs and preferences:

In India, the unpredictability of fire-related disasters calls for vital shields to address destruction, business interruption and associated damages. Instead of delving into a policy type that offers compensation for the expenses involved in reconstructing and repairing the wreck, know more about it from an insurance broker. The professional can guide you in attaining the ones with more coverage and ensure fair enough compensation for fire-related losses. Baid Inbest LLP is one of the best fire insurance brokers in the City of Joy. When seeking guidance related to this matter, seek the expertise of its professionals. It hardly matters if you represent an individual or a corporate entity; their brokers are ready to protect you against financial losses by comparing the most suitable policies and recommending the best to cover property restoration costs.

0 Comments

Back to Blog

Introduction

Travel insurance is like a dependable buddy who is always there for you if something goes wrong on your trip. However, given the multitude of possibilities, selecting the right policy from an insurance company might be difficult. But don't worry, we've got you covered! We've compiled some useful advice for selecting the best travel insurance. So, in this blog, we will discuss how to select insurance from a travel insurance company. Five Essential Tips for Choosing Travel Insurance

Ready to embark on your next adventure? Ensure a worry-free journey with the right travel insurance. Follow our five essential tips for choosing the perfect policy. And for the best travel insurance in India, look no further than Inbest LLP. With comprehensive coverage and peace of mind, your travels will be unforgettable for all the right reasons. Don't leave home without it!

Back to Blog

SIP Introduction

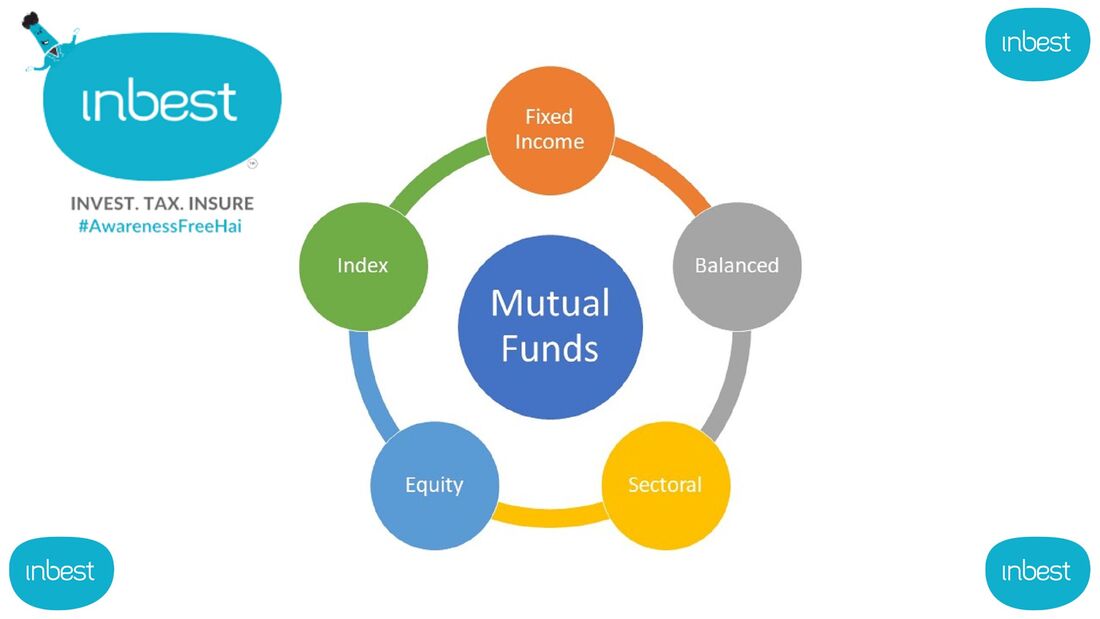

One of the most common investment options available to the public in India is mutual fund investing. In addition to lump-sum investments, one can use a variety of systematic procedures with money, such as SIP, STP, SWP, etc. Investors who are unfamiliar with these ideas or the distinctions between Systematic Investment Plan (SIP), Systematic Transfer Plan (STP), and Systematic Withdrawal Plan (SWP) may be confused by the terminologies. So, in this blog, we will explain these terms and discuss the key differences between SIP and STP. Read on! Systematic Investment Plan: What Is It? SIP is a disciplined investment strategy in which a person makes periodic fixed investments in their selected mutual fund scheme. These intervals can be monthly, fortnightly, quarterly, or any other frequency type that is currently accessible. SIPs are regarded as a goal-based investment strategy because they are frequently cited in equity mutual funds. It offers fantastic opportunities for people to invest in the equity markets with as little as Rs. 500 (or, in some situations, Rs. 100). Before making an investment decision, it is advised to look over the list of the top SIP plans. Systematic Withdrawal Plan: What Is It? In contrast to a systematic investment plan, a systematic withdrawal plan, or SWP, operates. Individuals are permitted to redeem fixed sums from mutual fund schemes under the SWP method. The investor first buys a few units of a mutual fund scheme that typically has low risk (mainly liquid funds) while using the SWP technique. They then provide instructions for the regular redemption of a fixed sum from these schemes. As directed, SWP in mutual funds can be carried out weekly, monthly, or every three months. Most retirees who require a consistent income prefer this strategy. Systematic Transfer Plan: What Is It? A systematic transfer plan allows investors to give mutual funds permission to systematically transfer a specified sum or redeem specific units from one scheme and invest in another scheme from the same mutual fund house. So, an amount or number of units chosen by an individual investor is moved from one mutual fund scheme to another regularly. As a result, this capability aids in the deployment of money at regular intervals. In other words, this is an automatic method of shifting money from one mutual fund to another. This plan is ideal when an individual wishes to invest a large sum yet wishes to minimise market timing risk. Difference Between a Systematic Investment Plan and a Systematic Transfer Plan While both STP and SIP entail regular contributions to equity mutual funds, the money for SIP comes from your bank account, whereas the money for STP comes from your debt fund. Also, since you are receiving returns from your debt fund, STPs provide larger yields than SIPs. Debt funds do not have the same solid rate of return as equity funds. But they generate decent returns of roughly 8% and are similarly immune to market volatility. You get the benefit of debt fund returns with STP. In the case of a systematic investment plan, the bank account offers a relatively low-interest rate. Therefore, you do not gain from that. Third, SIPs are typically unrestricted. The investment period is not predetermined. You are free to make withdrawals whenever you want and invest for as long as you wish. STPs are an exception to this. Both the quantity and the duration of the transfers are regulated. You must select the duration of the transfer, such It can be any numbers of Months. Final Words Inbest offers a range of systematic approaches, including SIP, STP, and SWP. A systematic investment plan is ideal for disciplined equity investments, while a SWP suits those seeking regular income. On the other hand, STP allows for strategic fund transfers. Each has its own unique characteristics, making it essential for investors to understand their goals and risk tolerance before choosing the most suitable option for their financial journey.

Back to Blog

Have you all heard of the new tax regime? Implemented on April 1, 2023, the fresh legislation robs people making debt fund investments of indexation benefits. It applies only to specific funds where equity investments fail to surpass 35% of their assets. Do you know what it implies? Mutual funds and bank FDs are more or less the same now! Both will be taxed in the same way. The silver lining to this cloud is that debt mutual funds will continue to offer tax benefits, making them more attractive to FDs. Let's examine the specifics and see what the issue is really about.

Tax Benefits of Debt Mutual Funds It seems debt funds are hard to compete with. Despite losing out on long-term capital gains (LTCG), they still lead the way, leaving bank FDs behind. The tax benefits they offer are listed and elaborated below:

The case of debt fund investments is slightly different though. As long as the debt mutual fund is untouched, capital gains tax incidence will not occur. Only when it is redeemed or transferred to a different mutual fund scheme will the capital gain tax be due. The only exception is in the event of a dividend payout under a debt-oriented fund scheme. The tax applied will be at the marginal tax slab rate. In other words, the tax due on debt MFs may be postponed.

One of the biggest advantages of debt MFs is that you can carry forward capital losses to other financial years and lower your taxable income. However, there is a distinct method of doing so as per the income tax laws. Let us explain through an example where there is a capital loss from debt MFs. Let’s say you incurred a capital loss of INR 30,000 from debt mutual funds and gains of INR 80,000 from equity shares. Your taxable income will now be INR 50,000 at the income tax rates applicable on the income slab. The capital gains will drop. Likewise, you may encounter a situation where losses from debt MFs surpass aggregate capital gains. Situations similar to this one will allow the individual to carry forward the capital losses for a maximum of seven assessment years, as long as the loss amount is hard to counterbalance in a financial year. What if there is a capital gain from debt MFs? In these circumstances, the short-term capital gain can be utilised to make up for any short-term losses on other assets. Likewise, long-term capital gains can set off long-term losses. Knowing the Tax Rules for Counterbalancing Gains/ Losses Capital gains ensuing from the sale or transfer of certain mutual funds are called short-term capital gains. According to the new tax rule, implemented on April 1, 2023, when calculating a taxpayer’s income, short-term capital gains will be counted, and income tax rates will apply to them regardless of the holding period. Here, ‘certain’ implies those debt MFs with equity investments not exceeding 35% of assets under management (AUM). The new tax laws will not apply unless the investment was made before April 1, 2023. Do you now realise why debt mutual funds are still the preferred choice over bank fixed deposits? Despite the dearth of LTCG indexation benefits, the prior is more attractive compared to the latter. For more such updates, visit Baid Inbest LLP to enlighten yourself.

Back to Blog

Everything you need to know regarding debt mutual funds

Introduction A debt fund is a specific class of mutual fund that invests in debt securities, such as corporate debt securities, corporate and government bonds, money market instruments, etc. Debt mutual funds come in a variety of forms to accommodate investors with various risk-return profiles, time horizons, and financial objectives. Treasury bills, government securities, commercial paper, certificates of deposit, money market instruments, securitized debt, and corporate bonds are just a few of the several types of debt that debt funds invest in. It is also referred to as bond funds or fixed-income funds. The primary difference between debt funds and equity funds is their investment in various asset types. Debt funds primarily hold bonds and cash assets, whereas equity funds allocate at least 65% of their assets to equities and equity-linked products. Remember that the values of the securities that comprise an investment determine its worth. Debt funds investment values are more steady than equity fund values due bond prices are often less erratic than stock prices. Therefore, money invested in debt is seen as less dangerous, especially when kept for brief periods of time. Why should you invest in debt funds? Debt funds have significant advantages for those investors who have always kept their money in bank accounts.

The Accrual Strategy of Debt Funds invests in bonds and holds them till maturity to produce consistent returns for the investor. This approach is centred on earning interest from the Bonds it buys. These Debt Funds have a relatively minimal interest rate risk since they retain investments until they mature. Liquid Funds, ultra-short duration funds, Low Duration Funds, and Money Market Funds are the main beneficiaries of this tactic. If you are looking to make debt fund investments that use this method, you should do so if you want steady returns with little risk. Wrapping Up Debt mutual funds provide investors with a range of benefits and opportunities. Investing in debt securities, like money market instruments and money, offers access to market returns and expertise. These funds also help reduce portfolio risk compared to equity funds. Investors can choose funds based on their preferred duration and credit risk, with various options for investing. Overall, debt funds offer a stable and potentially rewarding investment avenue for those seeking steady returns with lower risk.

Back to Blog

Introduction Wealth management plays a crucial role in helping individuals and families effectively grow, preserve, and distribute their wealth. Within the realm of wealth management, investment companies serve as valuable partners, providing expertise, guidance, and a range of investment solutions. What is an Investment Company? An investment company is an entity, such as a corporation or trust, that specializes in pooling the capital of investors to invest in financial securities. It commonly operates through closed-end funds or open-end funds, also known as mutual funds. Closed-end funds have a fixed number of shares and trade on exchanges, while open-end funds issue new shares continuously. These investment companies employ professional managers who make decisions on behalf of the shareholders, aiming to generate returns and diversify risks. They provide individuals and institutions with the opportunity to invest in a diversified portfolio of securities, regardless of their level of expertise or available capital and also let the clients know of the best investment plan. What is wealth management? Wealth management encompasses the process of creating and preserving wealth, involving a team of experts who assess the financial requirements of clients and recommend suitable financial products. This comprehensive approach includes safeguarding wealth, managing risks, accumulating assets, strategically positioning wealth, and eventually distributing it. With a focus on long-term wealth creation, wealth management aims to generate income from the asset base. It offers a broader scope of services to address various aspects of financial well-being and help individuals achieve their financial goals through tailored strategies and personalized advice. The Significance of Wealth Management Wealth management is vital for financial security, goal achievement, and peace of mind. It enables you to lay a solid foundation, defend against risks, and move towards your targeted milestones. By balancing income, expenses, and investments, effective wealth management allows you to retain your preferred lifestyle. It involves risk management through diversification and contingency preparation. Furthermore, successful wealth management enables legacy planning, ensuring that your assets are passed according to your preferences, and minimising tax responsibilities. By actively managing your wealth, you gain a sense of stability and confidence in your financial future. It brings peace of mind, knowing that you have a strategic plan in place to navigate financial challenges and preserve your financial well-being. How Investment Companies Can Contribute to Wealth Management? Investment companies play an important role in wealth management by offering a variety of investment choices and services to people and organisations. Here are a few instances of how investment firms help in wealth management:

Bottom lineInvestment companies play an important role in wealth management by offering a variety of investment options, knowledge, risk management measures, specialised investment strategies, and helpful advice to individuals and institutions. Investment companies help investors to diversify their portfolios and perhaps build their wealth over time by providing a wide range of investment options. The knowledge of these firms' professionals helps clients in making sound financial decisions, while risk management approaches limit potential investment hazards. With customized investment strategies and educational resources, investment companies contribute to the overall success of wealth management, helping individuals and families achieve their financial goals and secure their financial future.

Back to Blog

Mutual Funds Distribution in India is a complex process that involves a number of tax and insurance considerations. In order to ensure that you receive the most from your investment, it is important to understand the tax implications and insurance requirements associated with mutual fund distribution in India.

2. How are mutual funds distributed in India? Mutual funds are typically distributed through three different channels in India: 1. Direct selling: This is where investors buy mutual fund units from the fund house itself. There is no middleman and investors typically enjoy lower costs. 2. Regular distribution: This is where investors buy mutual fund units from an authorised distributor. These distributors may be banks, stockbroking firms or financial institutions. 3. Systematic investment plan (SIP): This is where investors buy mutual fund units on a monthly or quarterly basis. Units are purchased at a fixed price and investors typically enjoy lower costs. 3. What are the tax considerations for mutual fund investors? The tax considerations for mutual fund investors are many and varied. One of the most important is the timing of the sale of shares. For investors who hold shares in a taxable account, it is important to time the sale of shares to maximize the tax benefit. If the shares have been held for more than one year, the profit is considered a long-term capital gain, and is taxed at a lower rate than ordinary income. If the shares are sold within one year of purchase, the profit is considered a short-term capital gain, and is taxed at the investor's ordinary income tax rate. Another important consideration is the type of account in which the shares are held. For investors in a tax-deferred account, such as an IRA or 401(k), the profits on the sale of shares are not taxed until the account is withdrawn. This can be advantageous for investors who are in a higher tax bracket than the tax bracket in which the account is taxed. There are many other tax considerations for mutual fund investors, and it is important to consult with a tax professional to make sure that investors are taking advantage of all of the tax benefits available to them. 4. What are the insurance considerations for mutual fund investors? When investing in a mutual fund, it is important to understand the different types of insurance that are available to protect your investment. There are three types of insurance available: death, disability, and long-term care. Death insurance pays out a lump sum of money to your beneficiaries if you die. Disability insurance pays out a monthly benefit if you are unable to work due to an illness or injury. Long-term care insurance pays for nursing home care, home health care, or assisted living if you are unable to take care of yourself. It is important to understand that not all mutual funds offer insurance. You should check with the fund company to see if insurance is available. If it is, you will need to decide if you want to purchase it. The cost of insurance will depend on the amount of coverage you want and the age of the policyholder. Insurance can be a valuable tool to protect your investment, but it is important to weigh the costs and benefits before deciding if it is right for you. By understanding the tax and insurance considerations involved in mutual fund distribution in India, you can ensure that you receive the most from your investment. By working with a qualified financial advisor, you can make sure that you receive the best advice and guidance for your individual needs. |

RSS Feed

RSS Feed